Businesses and individuals often have to sign contracts when lending or borrowing money. These credit contracts protect them from financial losses and fines. The stipulations in credit agreements remain enforceable as long as both parties meet the conditions of the contract. But sometimes, when full debt repayment is impossible, the parties may come to a compromise by signing a debt settlement agreement.

In this article, we’ll discuss how a creditor can release an assignor from liability. But first, we’ll define a debt settlement agreement in detail.

What is a debt settlement agreement?

A debt settlement agreement is a legal contract signed between two parties in which one of them decides to relinquish a specific chunk of the total sum they are owed, provided the other party meets the demands of the contract.

In the business world, companies often default on loans due to improper management or unforeseen circumstances: case in point is COVID-19. So, instead of allowing the debtor to struggle to pay the total amount — which might lead them to bankruptcy — you could offer them the option to pay a certain percentage.

Although signing debt settlement agreements is not an obligation for every business transaction, doing so can help you avoid the risk of unsecured debts and unpayable loans. However, signing this agreement could lead to financial losses for the lender. That’s why you need to cover every important detail in the document before any assignment occurs.

Contents of a debt settlement agreement

Any standard debt settlement agreement should contain the following:

- Debtor’s (Assignor’s) details — the personal information of the entity that owes money to the creditor.

- Creditor (Assignee’s) details — the personal information of the entity that the debtor owes money to.

- Event — description of event, action, or circumstances under consideration.

- Date — the specific time and day when the agreement takes effect.

- Governing law — the governing body that will solve any disputes resulting from the agreement. This should contain the municipality, state, or country.

- Settlement amount — the amount receivable, including interests and the total repayable sums.

- Payment timelines — a specific time frame after which the contract becomes null and void, and the debtor has to pay the whole sum.

- Signatures — both parties need to sign their initials as well as provide handwritten or legally binding electronic signatures. If the debtor is in a different geographical location, you might also need to outline in the contract that signatures delivered electronically are part of the agreement.

- Terms of payment — the number of payments to be made, including the interest rate that will be charged.

The contract can also contain other information like modifications, insurance, right to an attorney, witnesses, addresses, phone numbers, and inclusion of force majeure, depending on the legal stipulations in your specific industry.

How can an assignor be released from liability?

Suppose you loaned $15,000 to a business owner before the pandemic, and projections show that they might not be able to stay solvent as they pay you back. In this case, you can reach an agreement with the debtor to stipulate how you want them to settle the debt.

That’s where the debt settlement agreement comes in. You (as the creditor) need to specify how much your debtor owes, how much you are willing to forgive, and the repayment conditions. For instance, you could ask the debtor to pay $7,500 (50%) within the coming six months. Once both parties sign the document, it becomes legally binding.

Who needs a debt settlement contract?

Companies and business owners that deliver high-risk services need a debt settlement agreement to avoid enormous financial losses. Individuals can also sign debt agreement contracts if the loans are secure: credit card loans, personal loans, medical bills, and student loans. However, you cannot use a debt contract for mortgages, car loans, and other types of secured loans.

Credit card companies also use debt agreements to forgive credit card debts to avoid cases where the cardholder decides to skip town without paying a dime. More so, if your business is close to bankruptcy and cannot service the loans or pay back your creditors, you can approach them with a debt settlement plan.

However, the drawback is that your card issuer may opt to close your account permanently at the end of the debt agreement contract. And for small and medium business owners, these debt contracts will affect your ability to secure loans in the future.

Tips for signing a debt settlement contract

Here are some things to know before signing a debt settlement agreement.

Use electronic release form waivers

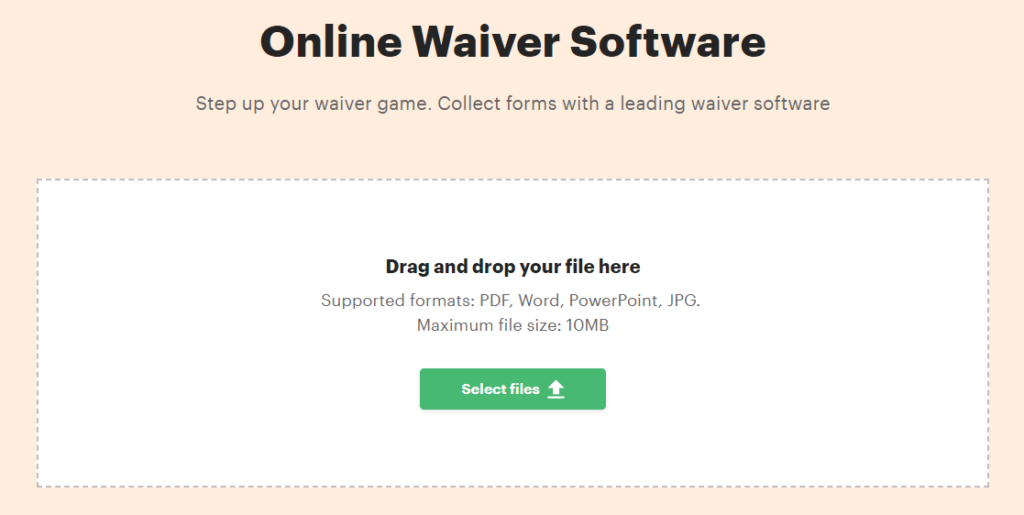

Electronic signatures are legally binding in the United States and European Union, provided they meet the criteria for legality. So instead of spending time printing out documents to sign, you can simply upload the contract and sign it online.

Online tools like the PandaDoc Waivers app provide a web interface where users can sign waivers instantly and securely. You just need to upload your debt release and sign it in a couple of clicks.

Be fair and transparent

When drafting the agreement, use clear language to describe the conditions for payment and other vital details. Using legal jargon to confuse the other party could land you in trouble for intentionally trying to mislead them.

In some cases, the debt agreement contract could be voided if it contains unfair conditions and/or unenforceable, illegal policies. No legal entity or government body will enforce such agreements, regardless of damages.

Hire legal help

As a general rule, always seek legal counsel before signing any waiver. These legal practitioners will review the contract’s fine print to ensure you get a fair deal. Also, you can assign the responsibility of extending the waived payment timeline to the legal counsel in cases of force majeure.

And most importantly, hiring legal consulting will help you cover all possible grounds that could cost your business in the future. For example, the lawyer will advise you if taking the debt settlement will affect your credit score as well as remind you that forgiven debt above $600 is taxable.

Conclusion

Whether you are a private individual or a business owner, you need to familiarize yourself with debt settlement contracts to protect your business from bankruptcy. When using a debt release agreement, make sure its content is comprehensive, concise, and legally binding before you start initializing it. If you have loads of debt agreement forms waiting to be signed, you can use our PandaDoc Waivers tool to expedite the process.